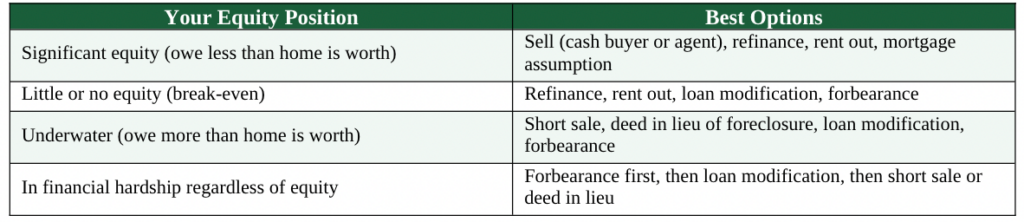

Getting out of a mortgage in Lincoln, Nebraska means different things depending on your situation. If you have equity, you have options ranging from a fast cash sale to refinancing. If you’re underwater on the loan or facing financial hardship, options like loan modification, forbearance, short sale, or deed in lieu of foreclosure may apply. This guide covers all five real ways Lincoln, Nebraska homeowners can exit a mortgage — not just the ones that benefit a single company.

Understanding What “Getting Out of a Mortgage” Means in Nebraska

A mortgage is a secured loan — your Lincoln home is the collateral. “Getting out” of that mortgage means either paying it off (through a sale or refinance), transferring it (through assumption or gifting with lender approval), or resolving it under hardship conditions (through modification, forbearance, short sale, or deed in lieu). The right option depends on one key question: how much equity do you have in your Lancaster County home?

How Much Equity Do You Have in Your Lincoln Home?

Equity is the difference between your home’s current market value and what you owe on the mortgage. To estimate it, contact the Lancaster County Assessor’s office for your assessed value, or request a comparative market analysis from a local Lincoln real estate agent.

Nebraska Mortgage Types — Which Options Are Available to You?

Your mortgage type determines which exit strategies are available. FHA loans allow assumptions and have specific forbearance rules through HUD. VA loans have their own modification programs through the Department of Veterans Affairs. USDA Rural Development loans — common in Lancaster County — have their own servicing guidelines. Conventional Fannie Mae and Freddie Mac loans follow CFPB guidelines for forbearance and modification.

Way #1: Sell Your Lincoln Home — Cash Buyer or Agent

If you have equity in your Lincoln, Nebraska home, selling it is the fastest and most complete way to pay off your mortgage and walk away with cash. You have two primary paths: sell to a local cash buyer for speed, or list with a Lincoln real estate agent for maximum net proceeds.

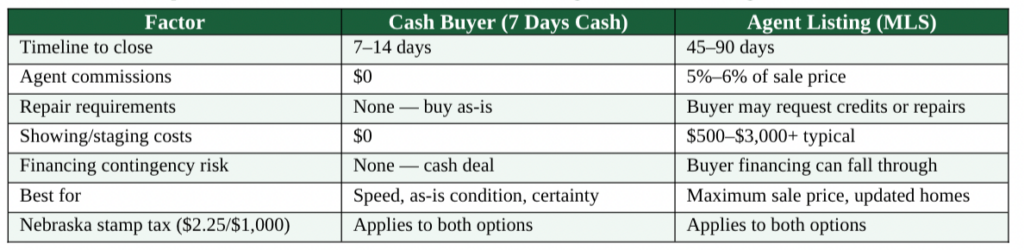

Option A: Sell to a Local Lincoln Cash Buyer — Close in 7 Days

A local cash home buyer purchases your Lincoln property directly, without financing contingencies, agent commissions, or repair requirements. The mortgage gets paid off at closing from the sale proceeds, and you receive the remaining equity in cash — often within 7 days of accepting the offer.

This approach works best when speed matters — divorce, job relocation, inherited property, pre-foreclosure, or a house that needs significant work. 7 Days Cash purchases homes directly in the Lincoln, Nebraska area including Lancaster County, Southeast Lincoln, Southwest Lincoln, and the Haymarket area, with no open houses, no staging, and no waiting for financing approval.

Option B: Sell with a Lincoln Real Estate Agent — Maximize Net Proceeds

Listing with a licensed Nebraska real estate agent on the MLS gives your Lincoln home maximum market exposure. This typically produces the highest sale price, but takes longer — the average days-on-market in Lincoln ranges from 20 to 60 days depending on price point, condition, and the time of year. Agent commissions in Nebraska typically total 5%–6% of the sale price.

If your home is in good condition, you have 60+ days, and maximizing your net proceeds matters most, a traditional listing is the right choice. For context on what affects sale timelines in Nebraska, see our guide: why Nebraska homes sit on the market and how to sell fast.

Cost Comparison: Cash Sale vs. Agent Listing in Lincoln, NE

Before you decide, read: how long does it take to sell a house in Nebraska to understand the full timeline.

Way #2: Refinance or Modify Your Mortgage

“Getting out” of a mortgage doesn’t always mean selling the house. If the problem is your current loan terms — a high interest rate, an ARM that reset, or unmanageable payments — refinancing into a new mortgage or modifying the existing one may resolve the issue without requiring a sale.

Mortgage Refinancing in Lincoln, Nebraska — When It Makes Sense

Refinancing replaces your existing mortgage with a new loan at a different rate, term, or structure. Nebraska homeowners refinance to:

- Lower a high interest rate (e.g., refinancing from a 7.5% to a 6% fixed rate)

- Switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage

- Extend the loan term from 15 to 30 years to reduce monthly payments

- Access home equity through a cash-out refinance

To refinance in Nebraska, you’ll need a current appraisal from a licensed Nebraska appraiser, sufficient equity (typically 20%+ for conventional, 3.5%+ for FHA), and qualifying credit score and income. The Nebraska Investment Finance Authority (NIFA) offers first-time homebuyer refinance programs that Lincoln residents may qualify for.

Loan Modification — For Lincoln Homeowners in Financial Hardship

A loan modification permanently changes the terms of your existing mortgage without requiring refinancing. Your lender may agree to reduce your interest rate, extend your loan term, or add missed payments to the end of the loan balance — all to make your monthly payment affordable again.

To apply for a loan modification in Nebraska, contact your loan servicer directly and request a hardship review. You will need to provide:

- Proof of financial hardship (job loss, medical bills, divorce, reduced income)

- Two months of bank statements

- Recent pay stubs or proof of income

- A hardship letter explaining your situation

Nebraska Housing Developer Association (NHDA) and HUD-approved housing counselors in Lincoln can provide free guidance on the modification process. This is a legitimate path to keep your home if temporary hardship is the issue.

Forbearance — A Temporary Pause on Payments

Forbearance is a temporary agreement with your lender to pause or reduce mortgage payments for a defined period — typically 3 to 12 months. It is not forgiveness; the missed payments must be repaid after the forbearance period ends (through a lump sum, repayment plan, or modification). However, forbearance provides immediate breathing room when a short-term crisis is the issue.

Contact your loan servicer directly to request forbearance. For FHA loans, HUD’s National Servicing Center handles this process. For VA loans, your lender works through the Department of Veterans Affairs. Forbearance does not require selling your Lincoln home and preserves your options for the next 3–12 months while you stabilize.

Way #3: Rent Out Your Lincoln Property to Cover the Mortgage

If you need to leave your Lincoln home — for a job, a relationship change, or a lifestyle decision — but aren’t ready to sell, renting the property is a way to keep the asset while having the tenant’s rent cover your mortgage payment.

Lincoln, Nebraska Rental Market — Is Your Property a Good Fit?

Lincoln has strong rental demand driven by the University of Nebraska-Lincoln (UNL) student population, state government employees, and a growing tech and healthcare sector centered around Lincoln’s innovation corridor and Bryan Health. Key Lincoln rental market data:

- Average 2-bedroom rent in Lincoln: approximately $1,050–$1,300/month (2024)

- Neighborhoods with highest rental demand: College View, Near South, University Place, Havelock

- UNL creates consistent August–May demand in the Near South and University Place areas

- Southeast Lincoln and Southwest Lincoln appeal to family renters and state employees

Before renting your property, verify that your mortgage is not a primary-occupancy-required loan (some FHA and USDA loans require owner-occupancy for a set period after origination). Also check Lincoln city rental licensing requirements and Lancaster County landlord-tenant law under Neb. Rev. Stat. § 76-1401 et seq. (the Nebraska Residential Landlord and Tenant Act).

Rent-to-Own in Lincoln — A Path to Sale With Monthly Income

A rent-to-own agreement (also called a lease-option or lease-purchase) allows a tenant to rent your Lincoln property with an option to purchase it at a pre-agreed price at the end of the lease term, typically 1–3 years. You receive monthly rent payments, a non-refundable option fee upfront, and the tenant is incentivized to maintain the property because they intend to buy it.

Key legal considerations for rent-to-own in Nebraska: the lease and option agreement must be documented in writing; the Nebraska Real Estate License Act requires that a licensed real estate agent or attorney prepare the option agreement if it’s presented as a real estate transaction. Consult a Nebraska real estate attorney before entering a rent-to-own arrangement.

Selling via rent-to-own works best when your Lincoln home has limited buyer pool at its current price, or when you need monthly income during a transition period. For an overview of what factors affect your home’s value in Nebraska, see: what reduces home value in Nebraska.

Way #4: Short Sale or Deed in Lieu — Options When You’re Underwater

If you owe more on your Lincoln mortgage than the home is currently worth — a situation called being “underwater” or having negative equity — selling at market value won’t pay off the full loan. In that case, two lender-approved options exist: a short sale or a deed in lieu of foreclosure.

What Is a Short Sale and How Does It Work in Nebraska?

A short sale occurs when your lender agrees to accept less than the full mortgage balance as payment in full, allowing you to sell the property at its current market value even though it’s below what you owe. The lender takes a loss; you avoid foreclosure on your credit report.

To pursue a short sale on your Lincoln, Nebraska property, you must:

- Demonstrate financial hardship to your lender (job loss, divorce, medical hardship, ARM reset)

- List the property with a licensed Nebraska real estate agent experienced in short sales

- Submit a short sale package to your lender — hardship letter, financial statements, comparative market analysis (CMA)

- Obtain written lender approval before accepting any buyer offer

Nebraska is a one-action state for mortgage deficiency judgments, meaning lender rights to pursue the deficiency balance after a short sale depend on whether the mortgage was a purchase money mortgage or a refinance. Consult a Nebraska real estate attorney before proceeding — this is a legal matter, not just a real estate transaction.

Credit impact: a short sale will appear on your credit report and may affect your score for 2–7 years. However, it is typically less damaging than a full foreclosure.

Deed in Lieu of Foreclosure — A Negotiated Alternative

A deed in lieu of foreclosure means you voluntarily sign the property title over to your lender in exchange for being released from the mortgage obligation — no foreclosure proceedings required. For Lincoln homeowners facing imminent default with no realistic path to catching up, a deed in lieu can be faster and less damaging than foreclosure.

To qualify, your lender must agree (they’re not required to accept a deed in lieu), the property must typically be listed and marketed for a set period first, and there must be no other liens on the property beyond the primary mortgage. A Nebraska real estate attorney should review the agreement — specifically, whether the lender is waiving their right to a deficiency judgment as part of the deed in lieu.

Way #5: Mortgage Assumption — Let Someone Else Take Over Your Loan

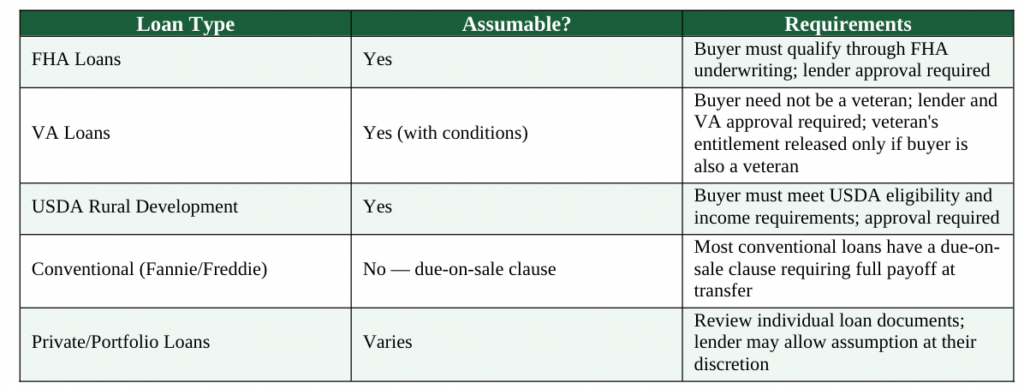

Mortgage assumption is a lesser-known but powerful option that lets a qualified buyer take over your existing mortgage — including its current interest rate, remaining balance, and terms — directly from your lender. For Lincoln homeowners with a below-market interest rate (especially FHA, VA, or USDA loans originated in 2020–2022 when rates were near historic lows), assumption can make your property highly attractive to buyers.

Which Mortgage Types Are Assumable in Nebraska?

Not all mortgages are assumable. Nebraska homeowners need to understand which loans allow assumption:

The Due-on-Sale Clause — What Lincoln Homeowners Must Know

Almost every conventional mortgage in the United States contains a due-on-sale clause (also called an acceleration clause). This clause gives the lender the right to demand full repayment of the loan when ownership of the property transfers. In plain terms: if you transfer title to a family member, gift the property, or sell it, the lender can call the entire loan balance due immediately.

This is the critical legal issue that many “Gift It” or “Transfer the Property” suggestions omit. Gifting a mortgaged property does not make the mortgage disappear. Unless:

- The loan is an assumable FHA, VA, or USDA mortgage and the recipient qualifies

- You are transferring to a spouse due to divorce (federal Garn-St. Germain Act exemption applies)

- You are transferring to an heir upon death (Garn-St. Germain exemption for inheritance)

- The lender explicitly approves the assumption in writing

…the lender can accelerate the loan when they discover the transfer. A Nebraska real estate attorney should review any mortgage transfer before it is executed.

Gifting a Mortgaged Lincoln Property — The Legal Reality

If you want to give your Lincoln home to a family member — a child, a sibling, or a parent — the process is legally complex when a mortgage is attached. You would need to either: (1) pay off the mortgage before transferring title, (2) obtain the lender’s written approval for the assumption, or (3) ensure the transfer qualifies for a Garn-St. Germain Act exemption (death or divorce situations).

Nebraska allows Transfer-on-Death (TOD) deeds under Neb. Rev. Stat. § 76-3401 et seq., which transfer real property to a named beneficiary automatically upon the owner’s death — without probate. However, a TOD deed does not transfer the mortgage, and the inheriting party becomes responsible for the balance. If they cannot assume or refinance, the property may need to be sold to satisfy the debt.

For more on Nebraska paperwork requirements for any home transaction, see: Nebraska home sale paperwork guide.

All 5 Ways Compared: Getting Out of Your Lincoln, Nebraska Mortgage

If Selling Is the Right Path: Why Lincoln Homeowners Choose 7 Days Cash

Not every option in this guide is right for every situation. If, after reviewing all five ways, selling your Lincoln home is the clearest path forward, working with a local Nebraska cash buyer removes the uncertainty of the traditional process.

7 Days Cash is a Veteran-owned, BBB A+-rated company that buys homes directly in the Lincoln, Nebraska market — including Lancaster County, Southeast Lincoln, Southwest Lincoln, and surrounding areas. We are not a national franchise, not a wholesaler, and not an algorithm. We are real local buyers who understand the Lincoln real estate market.

- We buy homes in any condition — no repairs, no cleaning required

- Zero commissions, zero agent fees, zero closing cost surprises

- We close on your timeline — 7 days or whenever you’re ready

- We handle all Nebraska paperwork, including the Nebraska Property Condition Disclosure Statement (Neb. Rev. Stat. § 76-2,120)

- We pay the Nebraska documentary stamp tax ($2.25 per $1,000 of sale price)

Learn how our home buying process works — three simple steps, no obligations.

Also see: Nebraska home buyers in 2026 — cash offers and fast sales for a full overview of your selling options in today’s Nebraska market.

Frequently Asked Questions About Getting Out of a Mortgage in Lincoln, Nebraska

Can I just stop paying my mortgage and walk away from my Lincoln home?

No — walking away without a formal agreement (short sale, deed in lieu, or foreclosure) results in foreclosure proceedings initiated by your lender. In Nebraska, mortgage foreclosures are judicial — meaning the lender files a lawsuit, a court enters a decree of foreclosure, and the property is sold at a sheriff’s sale. This process takes 6–18 months and results in a foreclosure on your credit report for 7 years. It is almost always better to pursue one of the 5 options in this guide.

How does Nebraska handle mortgage deficiency after a short sale or deed in lieu?

Nebraska law allows lenders to pursue a deficiency judgment for the unpaid balance after a short sale or deed in lieu unless the lender expressly waives the right in writing. This makes negotiating a deficiency waiver as part of the short sale approval or deed in lieu agreement critically important. Always have a Nebraska real estate attorney review the lender’s approval letter.

Are VA loans assumable for my Lincoln, Nebraska home?

Yes, VA loans are assumable in Nebraska with lender and VA approval, regardless of whether the buyer is a veteran. However, if the buyer is not a veteran, the original veteran’s VA loan entitlement remains tied to that loan and cannot be restored until the loan is fully paid off. If the buyer is a qualified veteran, a VA-to-VA assumption can restore the original borrower’s entitlement. Contact your VA loan servicer directly to initiate the assumption review process.

What is the fastest way to get out of a mortgage in Lincoln, NE?

For homeowners with equity, selling to a local Lincoln cash buyer is the fastest option — typically closing in 7–14 days with no repairs, no agent fees, and no financing contingencies. For homeowners in hardship, forbearance can be requested within days of contacting your servicer, providing immediate payment relief while you decide on a long-term strategy.

Does gifting my Lincoln house to a family member pay off my mortgage?

No. Transferring title to a family member does not extinguish the mortgage. If your loan contains a due-on-sale clause — which virtually all conventional loans do — the lender can demand immediate repayment of the full balance when they discover the title transfer. Exceptions exist under the federal Garn-St. Germain Act for transfers to spouses, children, and heirs upon death, but these exceptions are specific. Consult a Nebraska real estate attorney before transferring title on a mortgaged property.

What is a Nebraska Transfer-on-Death deed and does it eliminate the mortgage?

A Nebraska Transfer-on-Death (TOD) deed, authorized under Neb. Rev. Stat. § 76-3401 et seq., transfers real property automatically to a named beneficiary upon the owner’s death, bypassing probate. However, it does not eliminate or transfer the mortgage. The beneficiary inherits the property subject to the outstanding mortgage balance and must either assume the loan, refinance it, or sell the property to satisfy the debt.

Can I get out of my mortgage without selling my Lincoln home?

Yes — through refinancing (replacing your loan with a new one at better terms), loan modification (negotiating changed terms with your existing lender), or forbearance (a temporary payment pause). Mortgage assumption also lets a buyer take over your loan, effectively removing you from the obligation — but requires lender approval. Renting out the property keeps you as the owner while the tenant’s payments cover the mortgage.

Disclaimer: This article provides general information about mortgage exit options for Nebraska homeowners and does not constitute legal or financial advice. Mortgage law, lender requirements, and individual circumstances vary significantly. Consult a licensed Nebraska real estate attorney, a HUD-approved housing counselor, or a qualified financial advisor before making decisions about your mortgage.